CoreLogic®, a leading global property information, analytics and data-enabled solutions provider, today released the CoreLogic Home Price Index (HPI™) and HPI Forecast™ for February 2023.

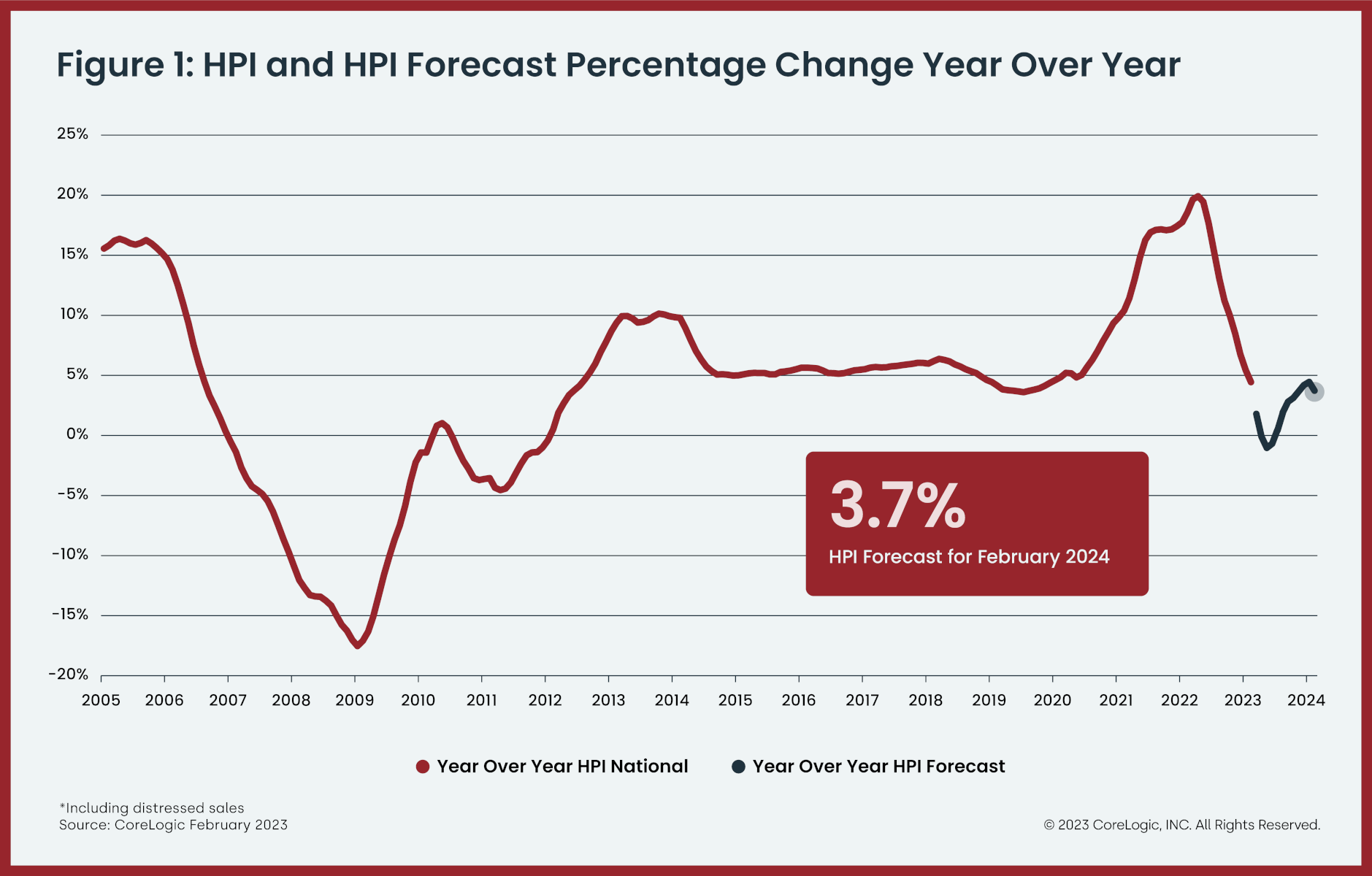

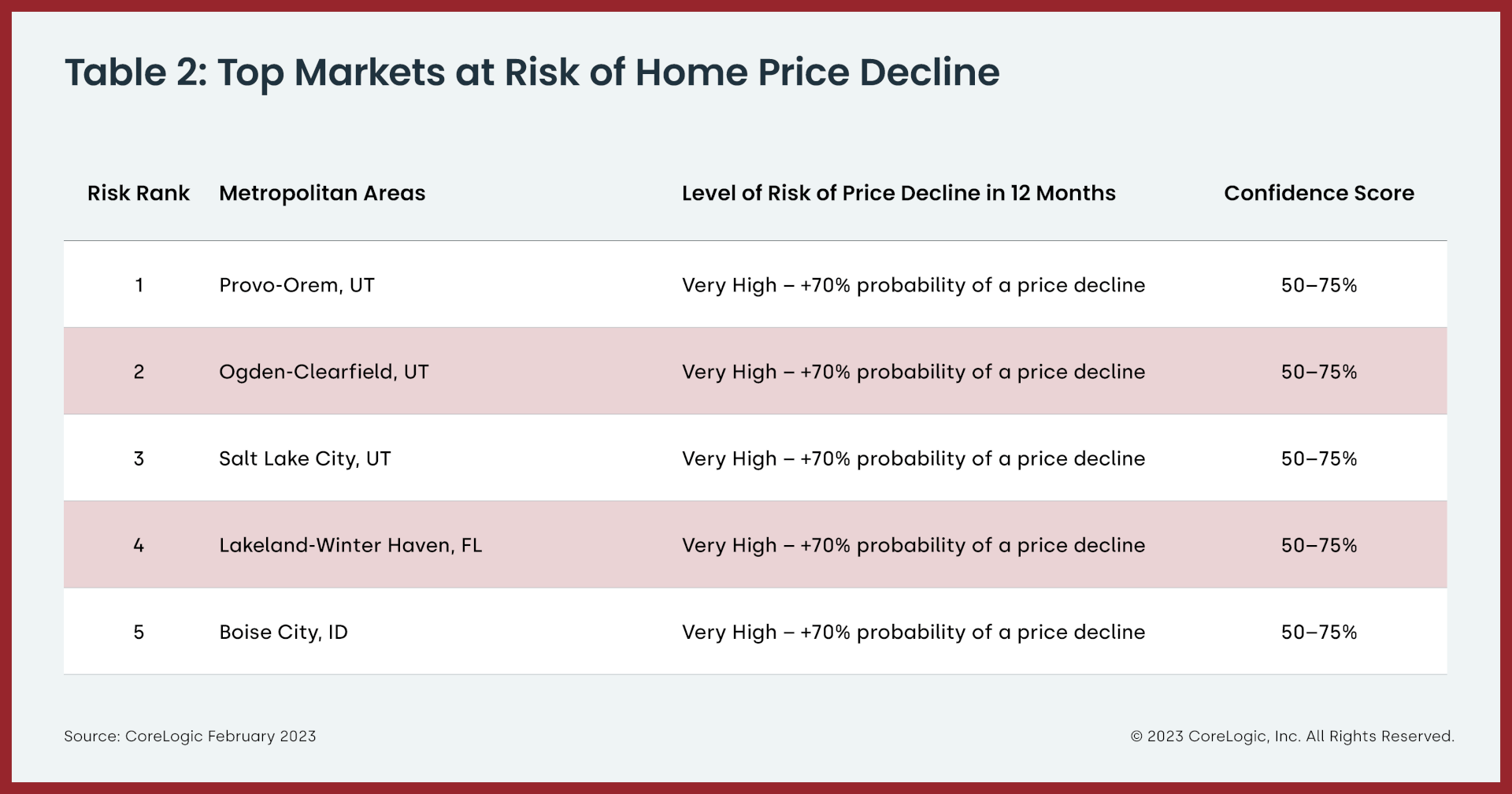

While annual U.S home price growth rose for the 133rd straight month in February, the 4.4% increase was the lowest recorded since 2019. Eight states and districts recorded annual home price losses, with much of the depreciation seen in the relatively expensive Western U.S., including California, Idaho, Oregon, Washington and Utah.

Tech company layoffs have likely affected housing demand on the West Coast, However, as noted in the latest CoreLogic S&P Case-Shiller Index, home prices gains are holding steady in some large East Coast metros, as workers return to offices and buyer demand renews in areas that saw relatively less appreciation during the pandemic. Areas in the Southern U.S. are also holding up well given current market conditions.

“The divergence in home price changes across the U.S. reflects a tale of two housing markets,” said Selma Hepp, chief economist at CoreLogic. “Declines in the West are due to the tech industry slowdown and a severe lack of affordability after decades of undersupply. The consistent gains in the Southeast and South reflect strong job markets, in-migration patterns and relative affordability due to new home construction.”

“But while housing market challenges remain, particularly in light of mortgage rate volatility and the ongoing banking turmoil,” Hepp continued, “pent-up homebuyer demand is responding favorably to lower rates in many markets. This trend holds true even in the West, leading to a solid monthly gain in home prices in February. U.S. home prices rose by 0.8% in February, double the month-over-month increase historically seen and indicating that prices in most markets have already bottomed out.”

Top Takeaways:

- U.S. home prices (including distressed sales) increased by 4.4% year over year in February 2023 compared to February 2022. On a month-over-month basis, home prices increased by 0.8% compared with January 2023.

- In February, the annual appreciation of attached properties (5.4%) was 1.4 percentage points higher than that of detached properties (4%).

- CoreLogic forecasts show annual U.S. home price gains slowing to 3.7% by February 2024.

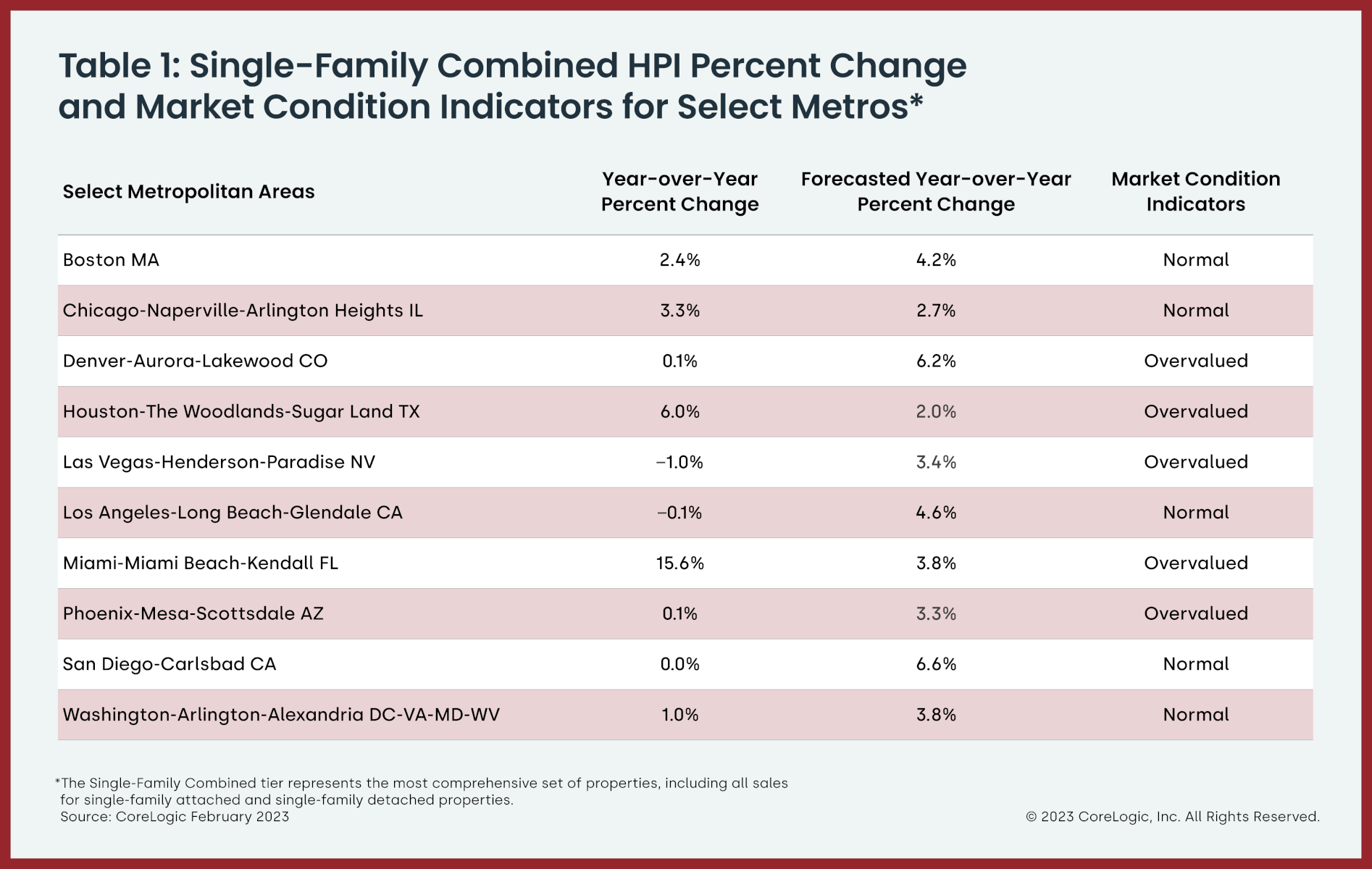

- Miami posted the highest year-over-year home price increase of the country’s 20 tracked metro areas in February, at 15.6%, while Tampa, Florida continued to rank second at 9.3%.

- Florida and Maine recorded the highest annual home price gains, 11.3% and 10.3%, respectively. South Carolina posted the third-highest growth, with a 9.2% year-over-year increase. Eight states and districts recorded annual losses: Washington (-4.9%), Montana (-3.1%), Nevada (-1.7%), Idaho (-1.6%), Utah (-1.6%), California (-1.5%), Washington, D.C. (-1.2%) and Oregon (-0.7%),

The next CoreLogic HPI press release, featuring March 2023 data, will be issued on May 2, 2023 at 8 a.m. EST.

Methodology

The CoreLogic HPI™ is built on industry-leading public record, servicing and securities real-estate databases and incorporates more than 45 years of repeat-sales transactions for analyzing home price trends. Generally released on the first Tuesday of each month with an average five-week lag, the CoreLogic HPI is designed to provide an early indication of home price trends by market segment and for the Single-Family Combined tier, representing the most comprehensive set of properties, including all sales for single-family attached and single-family detached properties. The indices are fully revised with each release and employ techniques to signal turning points sooner. The CoreLogic HPI provides measures for multiple market segments, referred to as tiers, based on property type, price, time between sales, loan type (conforming vs. non-conforming) and distressed sales. Broad national coverage is available from the national level down to ZIP Code, including non-disclosure states.